Inflation is rising: what might this mean for super balances?

Not a day goes past without a television talking head outlining the latest reason for sharp increases in prices. These price increases are due to a variety of causes and are affecting a wide range of goods and services that you and I use.

For example, the price of cars has jumped partly because of a worldwide shortage of computer chips; housing demand has risen due to cheap loans and COVID-driven migration; and we all know about toilet-paper, with supply plummeting due to moments of irrational panic buying, and opportunistic sellers marking up the value of the few rolls left. And the list goes on as we enter the post-pandemic era.

What’s this got to do with your super? Well, our focus is on increasing the value of your super investment so you're prepared for your life after work. But as prices rise your spending power is reduced. (I’ll explain below in more detail that this is something we actively work to manage by designing most members' investment options to beat inflation, which preserves the value of your super over time.)

In school we’re taught that some inflation is good as it encourages near-term spending. Over the long-term, inflation diminishes the relative size of any loan and can increase the value of growth assets. And real assets, such as commodities and real estate, are generally viewed as having excellent inflation-protection qualities. So it’s not all bad news, though you can get that impression from the media.

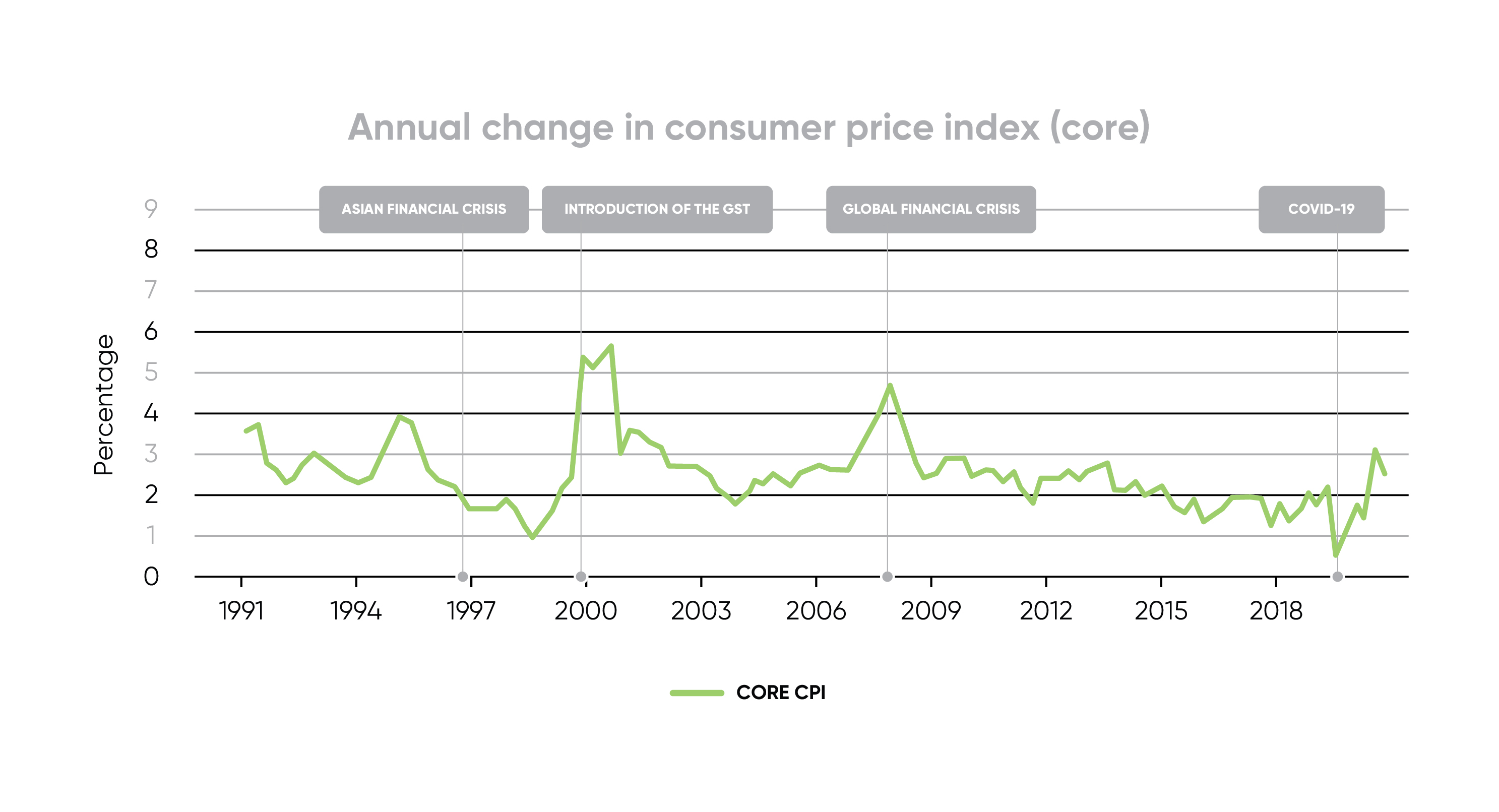

Source: Australian Bureau of Statistics, FactSet

But there are two types of inflation that cause problems: hyperinflation (very high inflation) which has a severe destabilising effect on the price of goods and services, and stagflation (high-price inflation and low-wage inflation) where our ability to pay for goods and services can’t keep up with escalating costs. These types of inflation are rare and, at least for now, don’t look likely to be seen in Australia.

How do governments influence the level of inflation?

Most reserve banks around the world view controlling inflation and employment/wage growth as central to their mission. Depending upon that country’s political drivers, other objectives may be in place, for example the Reserve Bank of New Zealand is particularly concerned about residential housing affordability.

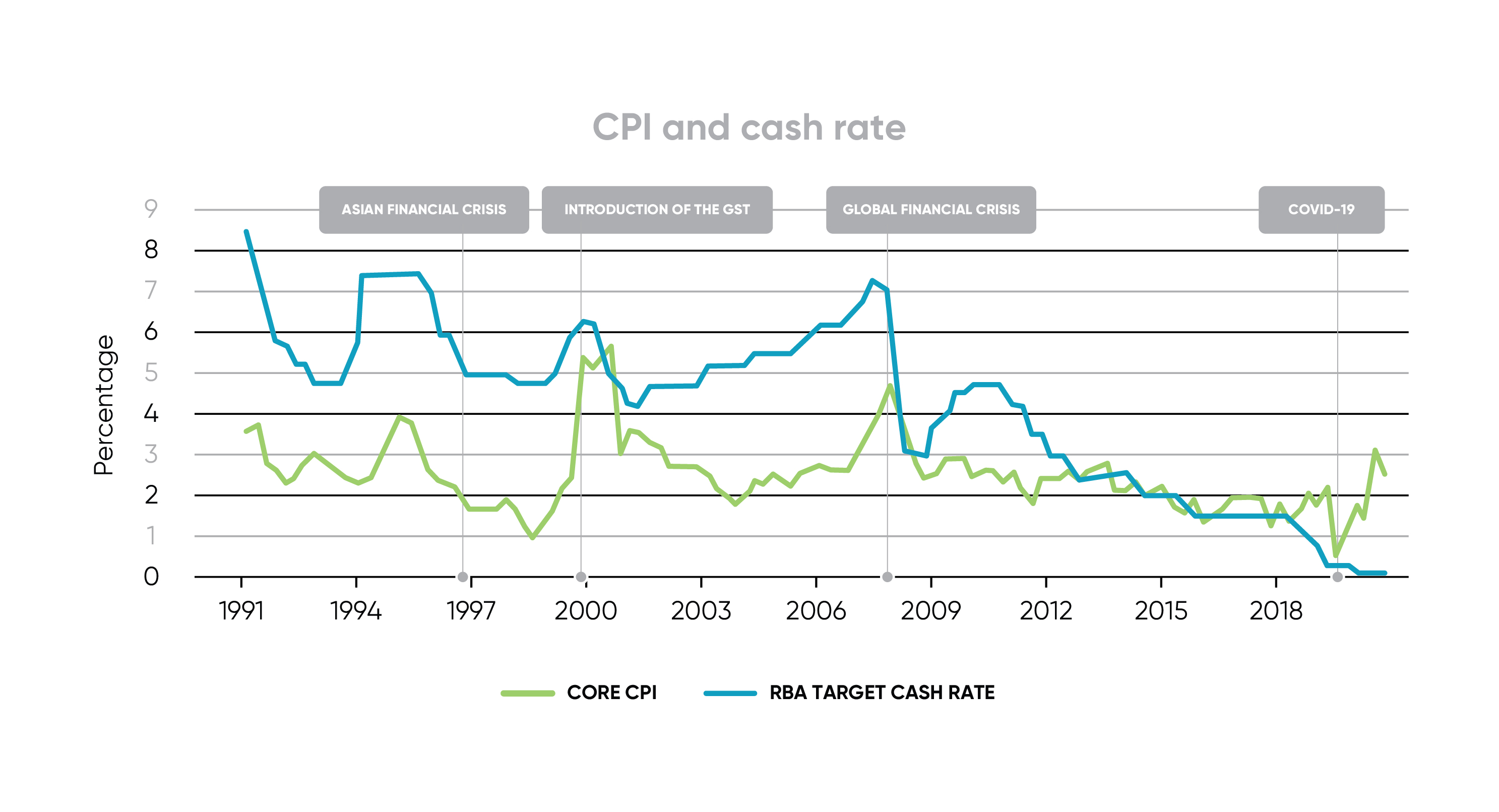

Interest rate change is the primary tool of reserve banks to clamp down or encourage inflation. The general idea is that higher rates stifle demand which eventually dampen inflation, while lowering rates has the opposite effect.

Australian interest rates have been moving downwards for more than 30 years. When shocks have occurred, such as last decade’s global financial crisis, the move down was sharp. Once risks subside, reserve banks look for opportunities to gradually move rates back to pre-crisis levels to stop inflation becoming too strong.

With the world recovering from the effects of COVID-lockdowns helped along by the stimulation of vast government spending and historically low interest rates, the risk of experiencing the wrong types of inflation is higher, while the risk of a further recession remains.

Our view is that reserve banks have deliberately risked delivering high-price inflation to avoid recession, and in addition their actions have (so far) generated mostly growth-asset value inflation rather than wage inflation. Pleasingly from a member perspective, asset price inflation is good for super balances, you just need to check out smartMonday’s gains from the past financial year to see that.

smartMonday super aims to beat inflation

Superannuation investing is, at its heart, about maximising your ability to spend in retirement. As inflation erodes the spending power of savings, many investment options are designed to return a couple of percent above inflation (known as the consumer price index or CPI).

The smartMonday options which most members invest in have inflation targets and are invested in a combination of growth assets that offer high returns which protect your investment from inflation or defensive assets that offer market-risk protection qualities.

Investing in growth assets is often the best way to beat inflation and increase your super balance over the very long-term. However, it is not always the right answer over the short-term, so we consider many different factors to navigate risks and generate strong returns, such as which companies are likely to retain profitability in a high-inflation environment.

Through such thinking the smartMonday investment team selects well diversified portfolios of securities to achieve the goal of the investment strategy. We monitor market conditions and vary the mix of securities frequently to navigate the risks and opportunities as they unfold.

Also, if you haven’t already done so, register for the member portal and check your current investment balance.

Want to know more?

Understanding the influence of inflation on investments is challenging. That’s why our smartCoach team is ready to provide you advice on your smartMonday super investments. There is no additional cost to use this service. You can contact our smartCoaches by:

- email: smartcoach@smartmonday.com.au

- phone: 1300 262 241