What you can expect from 2022

The world’s economic recovery from the pandemic should continue this year, albeit at a slower pace, despite inflation, war and the persistence of the coronavirus.

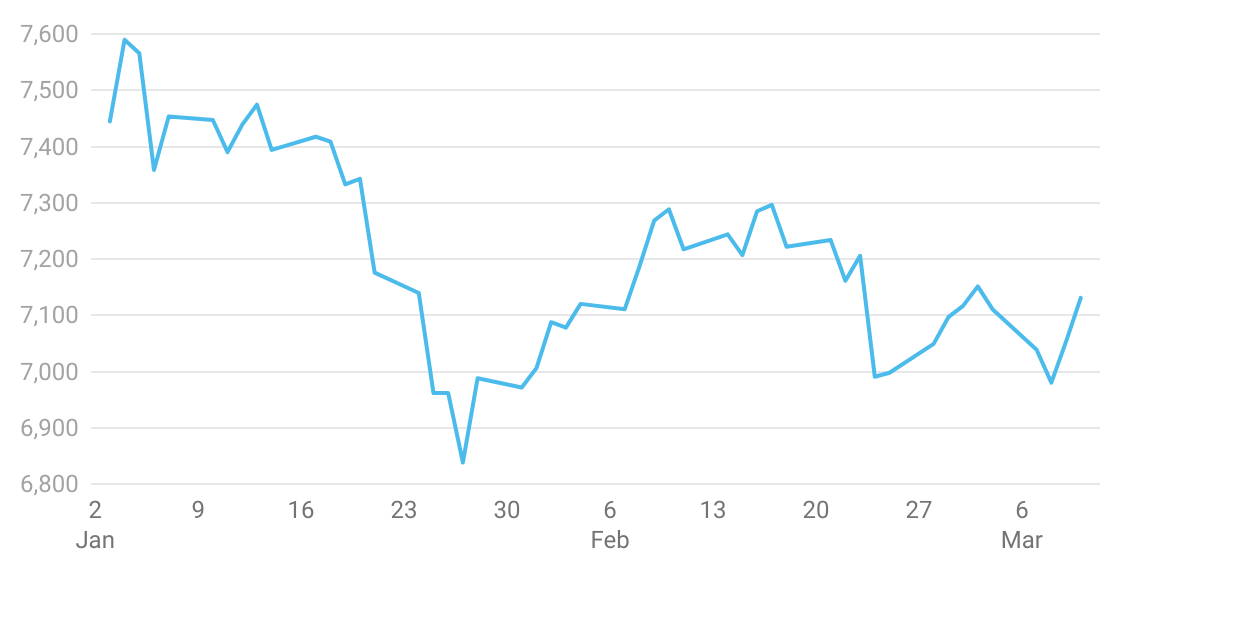

Last year’s stellar market performance, translating into exemplary gains for smartMonday members, hit turbulence almost as soon as 2022 began, with one of the local sharemarket’s most important indices, the S&P/ASX 200, falling 6.3 per cent in January – the biggest drop in about two years.

By February 11 most of that loss was regained. It goes to show that investors should always be cautious reacting too quickly when markets get volatile and their super balance drops. (The market has been up and down since February 24 due to investor reaction over Russia’s invasion of Ukraine.)

S&P/ASX 200 performance (Jan-Mar 2022)

January’s sharemarket pullback reflected the heady brew the markets ignored during the second half of 2021: low interest rates, contained inflation, improving economic activity, healthy profit margins, with government stimulus the cream on the top.

Of course, we don’t yet know how 2022 will pan out. There’s no way yet to predict if Russia’s invasion of the Ukraine will have a medium or long-term impact on market performance, but there are a few other interconnected issues emerging that will likely shape the year.

Invasion of Ukraine

The war in Ukraine is having a terrible impact on the daily lives of citizens caught up in the conflict. It remains uncertain it will develop, and given recent events, nothing can be ruled out. What is clear is that both the war and the uncertainty it causes are impacting investment markets, adding to volatility experienced so far in 2022.

Aside from the uncertain impact of the war itself, the global response from nations, companies and other organisations to exclude Russia from the global marketplace and economy will take some time to play out, pointing to more uncertainty.

There are two main forms to this action:

Government sanctions and other forms of market and economic exclusion, such as freezing financial assets of Russian elites and organisations, and withdrawal of goods and services from Russia by many companies from Apple to KPMG to McDonald’s.

Restriction of travel and trade for Russian people and goods by land and sea, which limits Russia’s economic ability to create export revenue.

At smartMonday, we have built diversified portfolios to cope with risky times. This means that while an event of the scale of the Russia-Ukraine war is negative for returns overall, we’re not exposed to significant loss related to owning Russian assets and companies.

smartMonday’s portfolio exposure to Russia's equity and bond markets is vanishingly small – to give you an idea, Russia comprises far less than 1% of our overall global equities exposure. There is also some indirect, but again very minor, exposure through smartMonday’s investments in multinational companies with Russia-based business operations and employees.

The pandemic

Another obvious issue is the ongoing pandemic: disruption from the surge of the omicron variant of COVID-19 has been significant close to home. The transition of Australia’s eastern states to a ‘living with covid’ approach late in 2021 enabled rapid spread in infections at the end of the year.

The quick spread of the omicron covid variant proves the continuing uncertainties around the global pandemic and remains a cautioning force on investors.

Inflation

The pandemic is the leading force pushing prices up significantly in some markets by disrupting the supply chains that deliver goods around the world.

Inflation – where the value of money lessens due to increasing prices of goods and services –hit a 40-year high in the US in the 12 months to the end of February 2022, with food, energy and real estate pushing the consumer price index up 7.5%. That’s on top of a 7% climb in December, according to US Bureau of Labor Statistics. (In Australia, underlying inflation is at a less scary 2.6% as of December 2021, according the Reserve Bank of Australia.)

Whether the inflation spike moderates further into 2022 is likely to be associated with how quickly supply chains normalise, but trends suggest there’ll be persistent price pressures well into the year.

Interest rates

Rapidly rising inflation is a big problem for central banks, who often raise rates to keep it under control. And when rates go up investors expect lower gains from ‘growth’ assets such as shares and property.

To date, many central banks around the world have said they’ll soon raise rates or that it’s on their agenda. Examples which are key to smartMonday portfolios are the Reserve Bank of Australia abandoning its stance of holding rates low until 2024 to declare it’ll possibly raise them this year; and the US Federal Reserve confirming rate rises there will begin soon, likely in March.

What it all means

Rate rises could have a big impact. We’ve had very low interest rates for several years, creating a positive environment for investors, such as superannuation account holders, where asset prices have risen significantly (the rise in residential property value and sharemarkets’ recent performance are prime examples).

So, if inflationary pressure persists, central banks will likely lift rates (and possibly rapidly), which could spook investors who will fear it’s going to get a lot tougher to make gains in the market. Investors may look for safer investment options and as they redirect their capital, markets could experience large losses.

Despite all the trends outlined above, 2022 is expected to be positive for global growth as the economic recovery continues, albeit in an unbalanced fashion. While 2021 was an exceptionally strong year in terms of sharemarket returns, it’s expected 2022 will be more moderate and volatile.

Given this expectation, we have already reduced risk in our portfolios by tapering back on Australian shares. We continue to build out our alternatives portfolios, favouring absolute return strategies in growth asset classes, and floating rate fixed-income securities in defensive classes.

Stay updated on your super’s performance

Take these three steps:

- Review recent articles on smartMonday’s performance

- Login to your account to see how your super has performed

- Speak with a smartCoach to see if your investments are on track for your goals