Investments gain as 2021/22 financial year begins

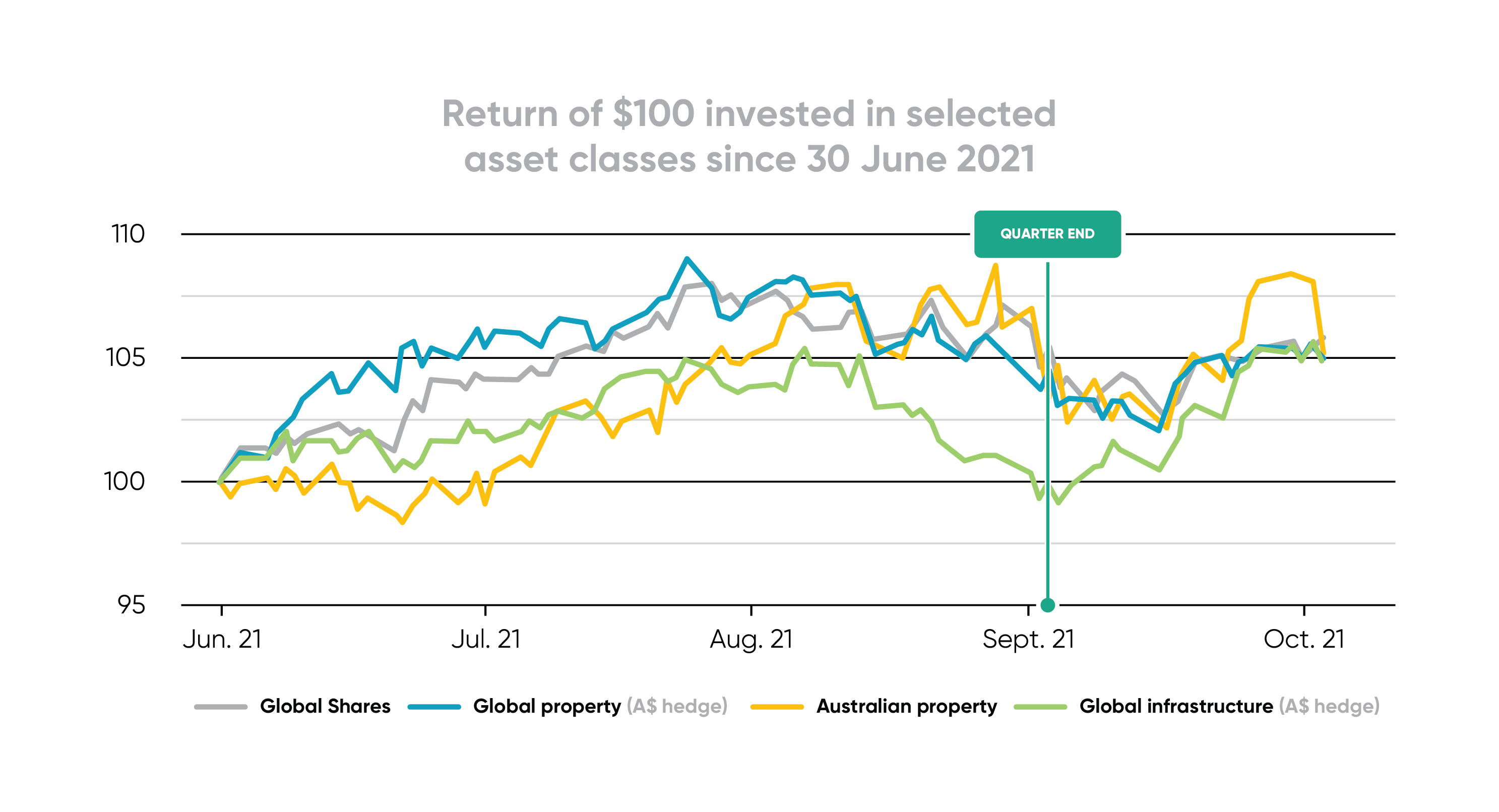

Almost all smartMonday members’ investments grew from July to September, driven largely by increasing value in shares and property.

This builds on very significant gains in most superannuation investments over the past financial year.

But before we discuss that further, let’s throw in a word of caution: there are some changes in the market that are making the smartMonday investment team more cautious as we look ahead.

Rising prices are one of these concerns, as they suggest we could be in for a period of inflation. While moderate inflation can be a welcome development, very high inflation that requires a strong response from reserve banks could work against further investment gains, or at least level them out.

But for the first quarter of this financial year most smartMonday investment options nudged upward, with our popular MySuper options all increasing 1% or more (as you can see in the table below).

smartMonday MySuper investment performance

Option

7 years (% p.a.)

5 years (% p.a.)

3 years (% p.a.)

1 year (%)

3 months (%)

MySuper age 35 and below

9.7

10.4

9.1

22.5

1.2

MySuper age 40

9.6

10.3

8.8

21.4

1.2

MySuper age 45

9.4

10.1

8.5

19.9

1.1

MySuper age 50

8.8

9.2

8.2

18.2

1.0

MySuper age 55

7.8

8.1

7.8

16.2

1.0

Notes: Performance shown net of investment fees and taxes. Past performance is not a guide to future performance. All data to 30 September 2021

Our sector specific options such as Property - Australian Index (up 4.4%) and International Shares - Index (up 3.7%) recorded the highest returns for the quarter. More defensive investment options saw smaller gains. You can review the performance of all our investment options here.

As always, keep in mind that superannuation is a long-term investment, and while it’s good to note what’s happening with your money each quarter and current market conditions, focusing on performance over several years, rather than months, gives you a clearer picture of gains you’re making, as you think about what you need for the future.

Market performance in detail

While growth assets performed well over the quarter, market attention has shifted to the threat of persistent high inflation and its implications for economic growth and monetary policy around the world.

Global sharemarkets outperformed Australian shares primarily due to the fall in the Australian dollar. China and other emerging markets – at earlier stages in their vaccination/reopening journeys and hence more vulnerable to growth slowdowns – were the weakest.

The Australian sharemarket’s modest performance masked significant sector dispersion – energy stocks boomed while materials tanked, reflecting sharp movements in commodity prices.

Asset class

Details

3 months %

1 year %

3 years p.a. %

5 years p.a. %

Growth assets

Australian shares

1.8

30.9

9.9

10.5

Australian property

3.9

27.8

13.2

15.1

Global property($A hedged)

4.8

30.7

9.2

7.7

Global infrastructure($A hedged)

3.0

29.1

6.2

5.7

International bonds ($A hedged)

-0.8

28.6

6.2

5.7

Defensive assets

Australian bonds

0.3

-1.5

4.1

3.1

International bonds ($A hedged)

0.1

-0.8

4.1

2.7

Data Source: FactSet based on representative market benchmarks. Past performance is not a reliable indicator of future performance. All data to 30 September 2021.

Energy resource prices surged driven by imbalance in supply and demand pursuant to global economic reopening, the iron ore price fell 40% reflecting the slowdown in China’s property construction and manufacturing sectors, dragging the performance of Australia’s major mining companies down with it.

Listed infrastructure and property asset classes experienced turbulent quarters. Rising bond yields weighed on both asset classes, with the infrastructure electricity-generation sector facing rising input costs due to the spike in energy resource prices.

After a solid start to the quarter most markets sold off in September, as you can see in the graph above, as investors were concerned the economic recovery was peaking, and inflationary pressures appeared more extensive and persistent than reserve banks initially expected.

The prospect of slower growth, higher inflation and higher interest rates undermined both growth and defensive assets late in the quarter, detracting from the strong performance of shares and real assets (like property). Global bonds finished relatively flat for the quarter as the prospect of tighter monetary policy in response to inflationary concerns drove bond yields higher.

Expectations that inflation and interest rates may rise

Inflation and economic growth concerns seem likely to dominate the headlines for a while to come. Key medium-term risks seem to be persistent high inflation (even if transitory, the longer it lasts, the more damage it could do to growth prospects), the prospect of aggressive tightening by reserve banks and contagion from China’s property development crisis.

To understand the risk is to understand the Chinese government’s resolve to achieve its policy objectives and stability, global inflation dynamics, and reserve banks’ determination to continue with monetary-stimulus strategies.

We believe China will do little more than what is necessary to avoid a disorderly collapse of its property-development sector. This will not stop the rapid slowing of the sector, resulting in lower Chinese economic growth as a whole and, importantly for Australia, less demand for iron ore and other key exports. Energy shortages leading to reported Chinese government-mandated manufacturing shutdowns adds to the negative outlook.

Expectation that higher inflation will persist through most of 2022 is increasing, despite reserve banks having claimed it would be transitory, though there’s a question mark on whether it extends beyond 2022. US headline inflation is a rising challenge, and the US Federal Reserve’s preferred core inflation measure is now more than 5% per annum (at a 30-year high) but our concern is more over what is underneath this. The worry is on several fronts: supply imbalances continue; inflation is broadening to more categories; and wages have been rising while labour shortages are still building. Already the US Fed has signaled it is likely to begin tapering asset purchases from November, and half of its policy-setting committee members now expect an interest rate increase in 2022.

In Australia, a major shift up in government bond yields seems to have surprised the Reserve Bank of Australia and caused it to abandon its target of keeping the cash rate at 0.1% until 2024. With interest rate increases a near-term possibility in Australia, it seems the Australian economy is past its stimulus peak, and the price of asset classes closely linked to the cost of borrowing (bonds and property) are now more challenged. More positively, the Australian population is well on its way to world-leading vaccination rates with lockdowns likely relegated to the past.

Investment outlook

Overall, our outlook for global risk assets has moderated since last quarter. While we do not believe large market falls are imminent, we expect some medium-term levelling out in the growth rate of the US sharemarket as some of its key longer term supports – high-profit margins and share buybacks, low inflation, and interest rates – start to turn.

The culmination of these factors leads us to favour a slightly underweight position in growth assets and to continue with our migration towards alternative investments that can withstand to offset equity market volatility – for example, we have earmarked an investment in direct global property.

In defensive asset classes we continue to hold fixed income as a downside risk control measure despite low prospective returns from the asset class. However, we are well-prepared for potential interest rate increases after having already diversified into new global credit strategies with higher incremental income, including floating-rate and insurance-linked securities, each having a lower correlation to the return of government bonds.

Is your super in the right investment strategy?

Here’s three steps to check:

- Review the performance of our investment options

- Login to your account to see how your super has changed

- Speak with a smartCoach to see if your investments are on track for your goals

*Based on APRA 7-year performance data for a high performing fund (9.44%) and a low performing fund (6.92%) and modelled with the ASIC superannuation calculator for a 28-year-old earning $60,000 a year, retiring at 67 years old